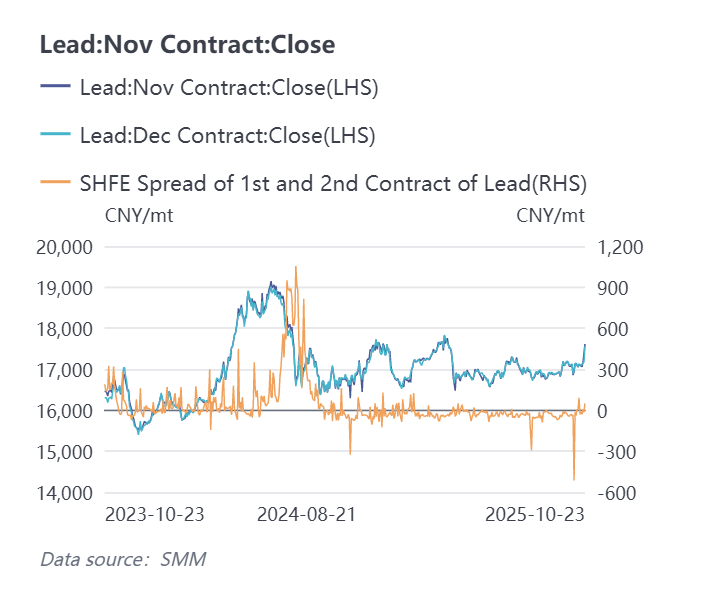

SMM October 23: SHFE lead prices surged strongly today, with intraday gains exceeding 600 yuan/mt, soaring to a high of 17,760 yuan/mt, the highest level in nearly seven months. As of the close at 15:00 on October 23, the SHFE lead 2511 contract settled at 17,615 yuan/mt, up 2.68%. Meanwhile, the SHFE lead market displayed a backwardation structure again after nearly nine months, with the spot-futures price spread between the 2511 and 2512 contracts reaching 140 yuan/mt (referencing the spread at the 11:30 morning close). The previous backwardation occurred in January 2025, with a spread of only 10-50 yuan/mt.

The sharp rise in lead prices was primarily driven by strong fundamental support.

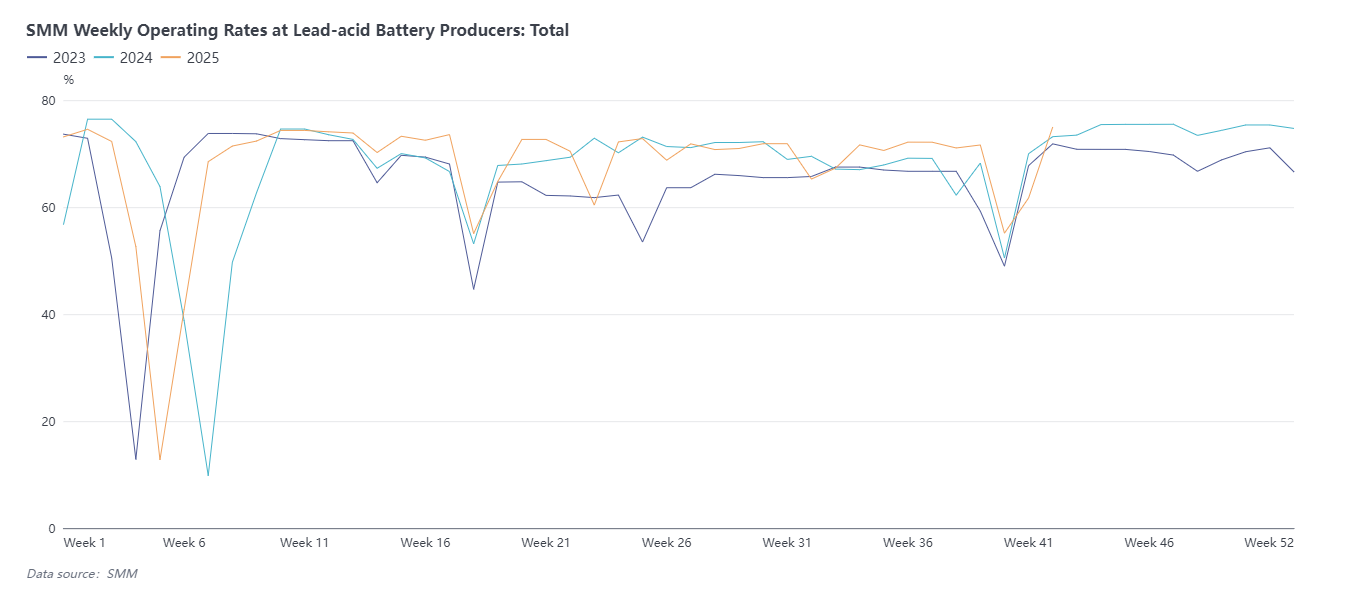

Firstly, lead consumption exceeded expectations. Due to the National Day & Mid-Autumn Festival holidays in October, lead-acid battery enterprises had holidays ranging from 0 to 8 days, with some even taking half a month. Meanwhile, downstream enterprises generally conducted routine stockpiling in September, pulling forward lead consumption, leading to expectations of weaker post-holiday consumption. However, after the National Day holiday, lead-acid battery enterprises resumed production as scheduled. Some enterprises, considering the traditional September-October peak season and Q4 consumption expectations, built inventories, leading to an increase in operating rates compared to pre-holiday levels. As of October 16, the weekly comprehensive operating rate for lead-acid battery enterprises in five provinces tracked by SMM was 74.97%, up 13.26 percentage points WoW and up 3.35 percentage points from pre-holiday levels (September 25).

Secondly, the pace of production resumptions at primary and secondary lead smelters has been slow, and vehicle transportation is restricted in some regions. Currently, primary lead smelters in north China, central China, northwest China, and other regions are undergoing maintenance or have not fully resumed production after maintenance due to undersupply of lead concentrates. Simultaneously, the production resumption pace for secondary lead smelters in regions like Anhui has been slower than expected, constrained by limited scrap battery supply and secondary lead profits hovering near the break-even line. Some enterprises have delayed their restart times from late November to the end of November. As of October 16, the weekly comprehensive operating rate for secondary lead enterprises in four provinces tracked by SMM was 35.1%, up 1.1 percentage points WoW.

Furthermore, starting October 15, some provinces and cities in north China began winter heating. This week, producers in regions like Hebei and Henan successively received notifications from higher-level environmental protection departments regarding controls on incoming vehicles, specifically prohibiting China V and below standard vehicles from entering plants. This has affected the transportation of materials like scrap and lead ingots for local primary lead smelters, secondary lead smelters, and lead-acid battery enterprises to varying degrees, lengthening transportation cycles.

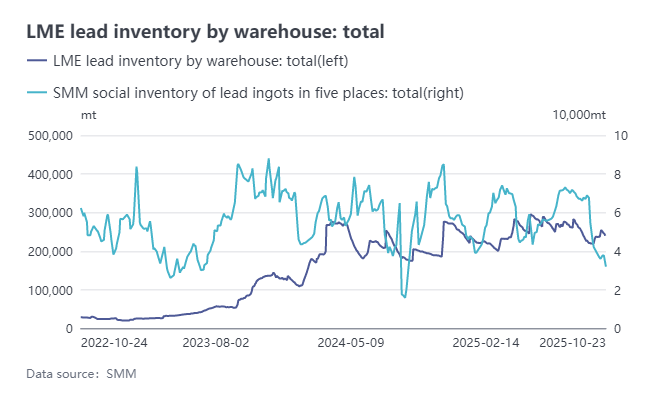

Finally, lead ingot inventory recorded a significant decline, with social inventory dropping to a new low in over a year. As of October 23, the total SMM lead ingot social inventory across five regions fell to 31,900 mt, down 5,700 mt WoW (October 16), reaching the lowest level since September 5, 2024. Recently, the operating rate of lead-acid battery enterprises stabilized with an increase, downstream enterprises actively made purchases, and smelter plant inventory in regions such as Henan and Hunan declined. Last week, SMM primary lead smelter plant lead ingot inventory was already below 3,000 mt. For instance, queuing for lead ingot cargo pick-up in Henan persisted from last week into this week, prompting some downstream enterprises to continue depleting lead ingot stocks in surrounding social warehouses, leading to a further decrease in social inventory.

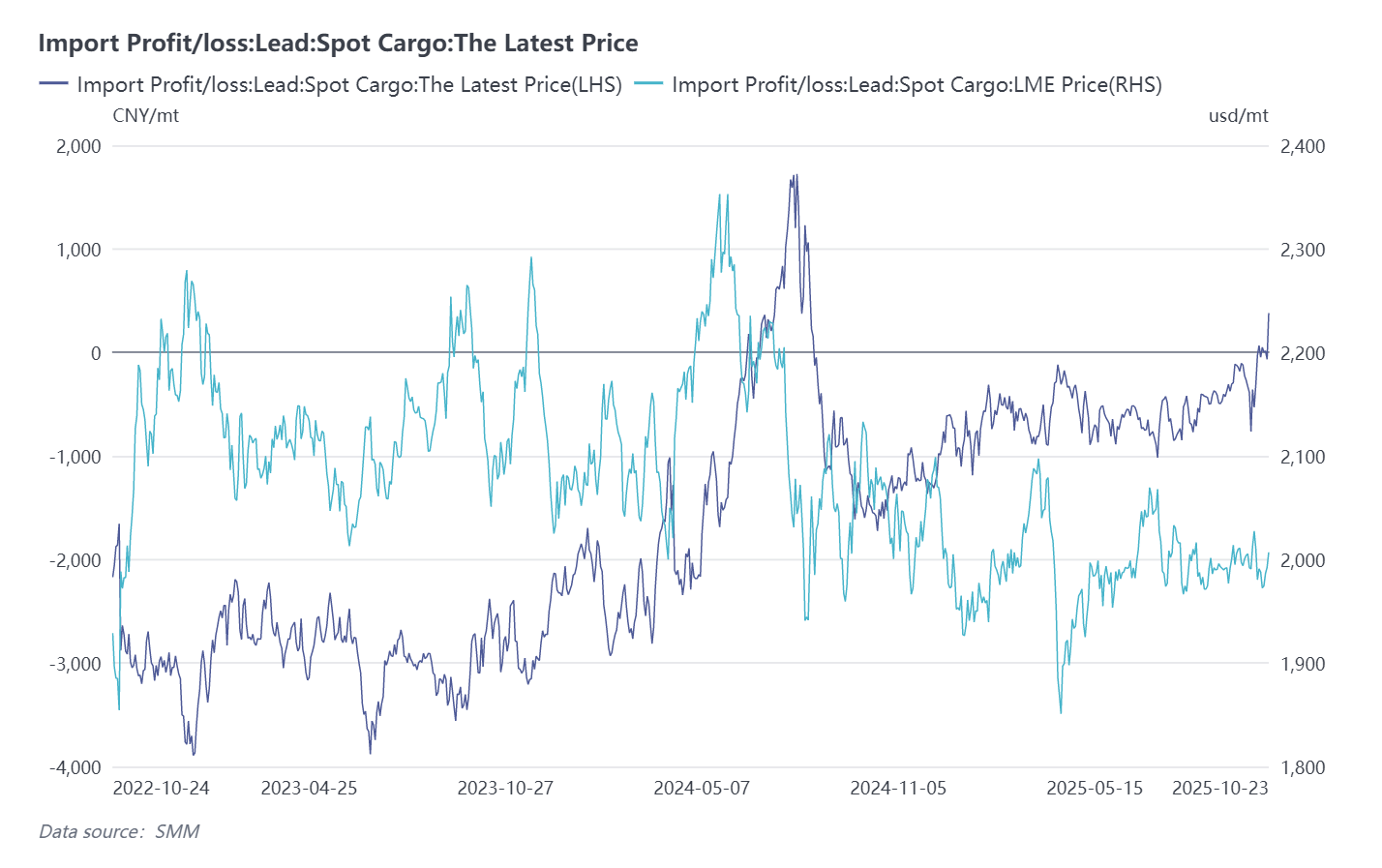

Additionally, it is important to note that domestic lead prices currently show stronger performance than overseas markets, and the import window for lead ingots is gradually opening, with expectations of increased lead ingot imports in the future. As of the SHFE lead closing on October 23, the profitability of lead ingot imports stood at 379 yuan/mt, with an intraday high reaching 573 yuan/mt (including a 3% import tariff). If lead ingots are sourced from countries with zero-tariff agreements, this profit margin would be larger. According to the latest LME inventory data, today (October 23) the total LME lead inventory was 239,700 mt, indicating favorable import conditions. In the short term, low lead ingot inventory will support prices to fluctuate at highs. If subsequent increases in lead ingot supply or imports materialize, lead prices face the risk of a retreat after a rapid rise.